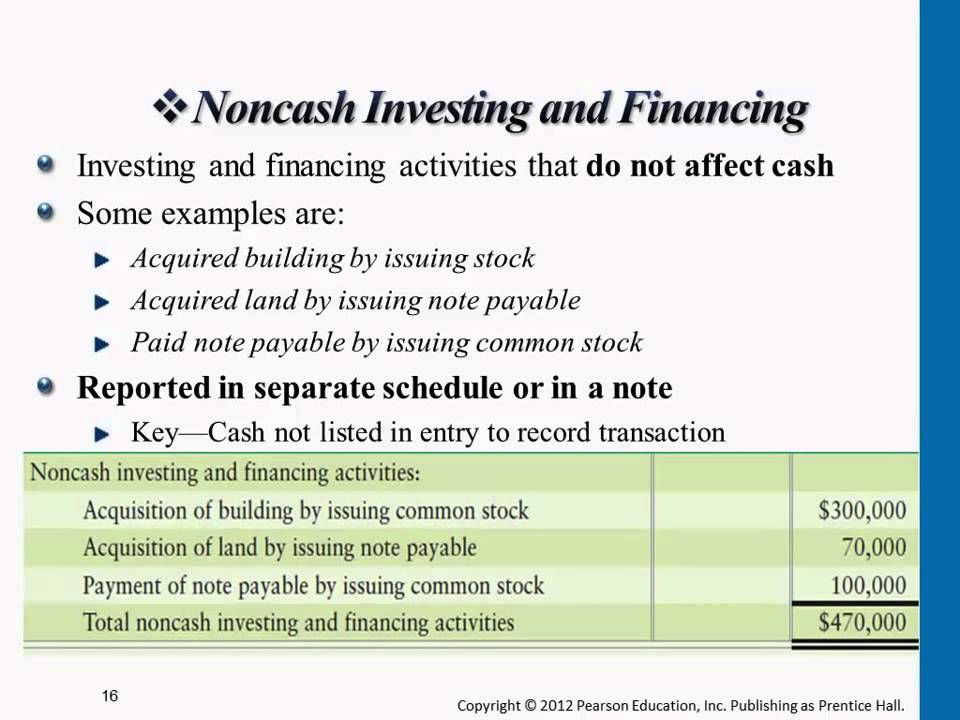

Where do the insurance companies invest?

Illiquid bonds: this is the preferred form of investment by insurance companies, which can thus count on predictable and stable cash flows over time. Given the high competitiveness of the sector, the return obtained is thus transferred to policyholders through a lower price for insurance

Insurance companies perform one of the most important forms of financial intermediation in modern society. Specifically, they allow households to share risk and protect themselves against the economic costs of accidents and injuries that would otherwise have devastating effects on peoples’ lives and savings. A less known side of insurance companies is that they are also major investors in financial assets. Given that insurance companies receive insurance premia immediately and only pay out in case of an accident later on, underwriting an insurance contract involves an investment decision: what should the insurance company do with money it receives for underwriting insurance contracts? In our paper, we investigate how the particular funding structure of insurance companies – the underwriting of insurance contracts – makes them ideal investors in illiquid corporate bonds. Further, we document how insurance companies’ investment strategies affect the price of insurance contracts faced by everyday consumers.

To understand the paper’s main insights, let’s discuss three key features of the insurance business. First, insurance companies underwrite many similar contracts in order to diversify their insurance portfolios. Diversification makes the aggregate cash flows generated by insurance underwriting predictable; we don’t know what specific house will catch fire, but the insurance company has a pretty good idea of the fraction of houses that will burn in a given year and how much they will have to pay to policy holders to fix damages. A second feature is that insurance demand is relatively stable; people tend to buy house insurance and car insurance in good times and bad times indifferently. This provides insurance companies with a stable source of funding which is less sensitive to market fluctuations than funding structures of other investors (e.g. mutual funds or banks). These first two features of the insurance business make insurance underwriting a stable and predictable source of funding for insurance companies.

The question is then what the insurance companies should invest in given their funding structure and the answer turns out to be illiquid bonds (Empirically we find that illiquid credit makes up more than 70% of US Life Insurers’ investment portfolios). Illiquid bonds are debt securities which can be hard to sell and therefore trade at a discount relative to their fundamental values. If you are an investor whose funding dries up when the market goes down, you don’t want to hold too many illiquid assets as you could be forced to sell them at a big discount. This is a well-known issue for open-end mutual funds and even banks that are vulnerable to so-called runs (hello, Silicon Valley Bank), but if you have stable funding you have an advantage. You can buy illiquid, but fundamentally sound, assets at a discount because you can commit holding these assets until maturity due to the stable nature of your funding; policy holders cannot claim their money back at will and houses won’t start catching on fire more than usual just because there is turmoil in bond markets. This means insurance companies, because of their stable funding, have higher expected returns on illiquid assets than other investors.

The third and final feature of the insurance industry is that it is competitive. Because insurance underwriting is a valuable source of funding, insurance companies compete to attract customers by setting lower prices. This means that part of the excess return that insurance companies can make by investing in illiquid bonds is being passed on to policy holders through lower insurance prices. We denote this mechanism asset-driven insurance pricing and document its presence across different insurance products and time periods.

In summary, we argue that insurance companies use their stable funding to earn excess returns on illiquid assets and pass back part of these excess returns to policy holders who are the source of stable funding. This implies that insurance premiums are lower when insurance companies have higher than expected investment returns because insurers compete for funding. In this way, insurance companies combine two very valuable forms of financial intermediation by buying assets when other investors are forced to sell, and by enabling risk-sharing amongst households and corporations at competitive prices.

Finance Chapter 2 Exercises

The story of Apple Computer provides three examples offinancing sources: equity investments by the founders of the company, tradecredit from suppliers, and investments by venture capitalists. Other sources include reinvested earnings ofthe company and loans from banks and other financial institutions.

Financial Markets. The stock and bond markets are not the only financial markets. Give two or three additional examples.

a) Investor A buys shares in a mutual fund, which buyspart of a new stock issue by a rapidly growing software company.

b) InvestorB buys shares issued by the Bank of New York, which lends money to a regionaldepartment store chain.

c) Investor C buys part of a new stock issueby the Regional Life Insurance Company, which invests in corporate bonds issuedby Neighborhood Refineries, Inc.

Financial Intermediaries. You are a beginning investor with only $5,000 in savings. How can you achieve a widely diversified portfolio at reasonable cost?

Buyshares in a mutual fund. Mutual fundspool savings from many individual investors and then invest in a diversifiedportfolio of securities. Each individualinvestor then owns a proportionate share of the mutual fund’s portfolio

Financial Intermediaries. Is an insurance company also a financial intermediary? How does the insurance company channel savings to corporate investment?

Yes, an insurance company is a financialintermediary. Insurance companies sellpolicies and then invest part of the proceeds in corporate bonds and stocks andin direct loans to corporations. Thereturns from these investments help pay for losses incurred by policyholders.

Corporate Financing. Choose the most appropriate term to complete each sentence. a. Households hold a greater percentage of (corporate equities / corporate bonds).

b. (Pension funds / Banks) are major investors in corporate equities.

c. (Investment banks / Commercial banks) raise money from depositors and make loans to individuals and businesses.

a. Equities.As a percentage of all investors, households are the largest investor in equities. b. Pensionfunds. Banks own almost no corporateequities, but instead rely on fixed- income investments.

c. Commercialbanks. In contrast, investment banks raise money for corporations.

Financial Markets. Which of the following are financial markets?

b. Vanguard Explorer Fund

c. JPMorgan Chase

d. Chicago Mercantile Exchange

NASDAQand The Chicago Mercantile Exchange are financial markets

Financial Intermediaries. True or false?

a. Exchange traded funds are hedge funds that can be bought and sold on the stock exchange. b. Hedge funds provide small investors with low-cost diversification.

c. The sale of policies is a source of financing for insurance companies.

d. In defined-contribution pension plans, the pension pot depends on the rate of return earned on the contributions by the employer and employee.

Liquidity. Securities traded in active financial markets are liquid assets. Explain why liquidity is important to individual investors and to mutual funds.

Liquidity is important because investors want to beable to convert their investments into cash quickly and easily when it becomesnecessary or desirable to do so. Shouldpersonal circumstances or investment considerations lead an investor toconclude that it is desirable to sell a particular investment, the investorprefers to be able to sell the investment quickly and at a price that does notrequire a significant discount from market value.

Liquidityis also important to mutual funds. Whenthe mutual fund’s shareholders want to redeem their shares, the mutual fund isoften forced to sell its securities. Inorder to maintain liquidity for its shareholders, the mutual fund requiresliquid securities.

Liquidity. Bank deposits are liquid; you can withdraw money on demand. How can the bank provide this liquidity and at the same time make illiquid loans to businesses?

Thekey to the bank’s ability to provide liquidity to depositors is the bank’sability to pool relatively small deposits from many investors into large,illiquid loans to corporate borrowers. Awithdrawal by any one depositor can be satisfied from any of a number ofsources, including new deposits, repayments of other loans made by the bank,bank reserves, and the bank’s debt and equity financingvel���MD��

Financial Institutions. Summarize the differences between a commercial bank and an investment bank.

Commercial banks accept deposits and provide financingprimarily for businesses. Investmentbanks do not accept deposits and do not loan money to businesses andindividuals. Investment banks may makebridge loans as temporary financing for a takeover or acquisition. In addition, investment banks trade manydifferent financial contracts, such as bonds and options, while providinginvestment advice and portfolio management for institutional and individualinvestors.

Mutual Funds. Why are mutual funds called financial intermediaries? Why does it make sense for an individual to invest her savings in a mutual fund rather than directly in financial markets?

Mutualfunds collect money from small investors and invest the money in corporatestocks or bonds, thus channeling savings from investors to corporations. For individuals, the advantages of mutualfunds are diversification, professional investment management, and recordkeeping

https://www.unibocconi.it/en/news/where-do-insurance-companies-investhttps://www.cram.com/flashcards/finance-chapter-2-exercises-8267856