98 Differentiate between Operating, Investing, and Financing Activities

The statement of cash flows presents sources and uses of cash in three distinct categories: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Financial statement users are able to assess a company’s strategy and ability to generate a profit and stay in business by assessing how much a company relies on operating, investing, and financing activities to produce its cash flows.

Classification of Cash Flows Makes a Difference

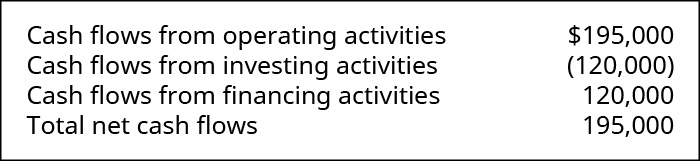

Assume you are the chief financial officer of T-Shirt Pros, a small business that makes custom-printed T-shirts. While reviewing the financial statements that were prepared by company accountants, you discover an error. During this period, the company had purchased a warehouse building, in exchange for a $200,000 note payable. The company’s policy is to report noncash investing and financing activities in a separate statement, after the presentation of the statement of cash flows. This noncash investing and financing transaction was inadvertently included in both the financing section as a source of cash, and the investing section as a use of cash.

T-Shirt Pros’ statement of cash flows, as it was prepared by the company accountants, reported the following for the period, and had no other capital expenditures.

Because of the misplacement of the transaction, the calculation of free cash flow by outside analysts could be affected significantly. Free cash flow is calculated as cash flow from operating activities, reduced by capital expenditures, the value for which is normally obtained from the investing section of the statement of cash flows. As their manager, would you treat the accountants’ error as a harmless misclassification, or as a major blunder on their part? Explain.

Cash Flows from Operating Activities

Cash flows from operating activities arise from the activities a business uses to produce net income. For example, operating cash flows include cash sources from sales and cash used to purchase inventory and to pay for operating expenses such as salaries and utilities. Operating cash flows also include cash flows from interest and dividend revenue interest expense, and income tax.

Cash Flows from Investing Activities

Cash flows from investing activities are cash business transactions related to a business’ investments in long-term assets. They can usually be identified from changes in the Fixed Assets section of the long-term assets section of the balance sheet. Some examples of investing cash flows are payments for the purchase of land, buildings, equipment, and other investment assets and cash receipts from the sale of land, buildings, equipment, and other investment assets.

Cash Flows from Financing Activities

Cash flows from financing activities are cash transactions related to the business raising money from debt or stock, or repaying that debt. They can be identified from changes in long-term liabilities and equity. Examples of financing cash flows include cash proceeds from issuance of debt instruments such as notes or bonds payable, cash proceeds from issuance of capital stock, cash payments for dividend distributions, principal repayment or redemption of notes or bonds payable, or purchase of treasury stock. Cash flows related to changes in equity can be identified on the Statement of Stockholder’s Equity, and cash flows related to long-term liabilities can be identified by changes in long-term liabilities on the balance sheet.

Can a Negative Be Positive?

Investors do not always take a negative cash flow as a negative. For example, assume in 2018 Amazon showed a loss of $124 billion and a net cash outflow of $262 billion from investing activities. Yet during the same year, Amazon was able to raise a net $254 billion through financing. Why would investors and lenders be willing to place money with Amazon? For one thing, despite having a net loss, Amazon produced $31 billion cash from operating activities. Much of this was through delaying payment on inventories. Amazon’s accounts payable increased by $78 billion, while its inventory increased by $20 billion.

Another reason lenders and investors were willing to fund Amazon is that investing payments are often signs of a company growing. Assume that in 2018 Amazon paid almost $50 billion to purchase fixed assets and to acquire other businesses; this is a signal of a company that is growing. Lenders and investors interpreted Amazon’s cash flows as evidence that Amazon would be able to produce positive net income in the future. In fact, Amazon had net income of $19 billion in 2017. Furthermore, Amazon is still showing growth through its statement of cash flows; it spent about $26 billion in fixed equipment and acquisitions.

Key Concepts and Summary

- Transactions must be segregated into the three types of activities presented on the statement of cash flows: operating, investing, and financing.

- Operating cash flows arise from the normal operations of producing income, such as cash receipts from revenue and cash disbursements to pay for expenses.

- Investing cash flows arise from a company investing in or disposing of long-term assets.

- Financing cash flows arise from a company raising funds through debt or equity and repaying debt.

Multiple Choice

(Figure)Which of these transactions would not be part of the cash flows from the operating activities section of the statement of cash flows?

- credit purchase of inventory

- sales of product, for cash

- cash paid for purchase of equipment

- salary payments to employees

(Figure)Which is the proper order of the sections of the statement of cash flows?

- financing, investing, operating

- operating, investing, financing

- investing, operating, financing

- operating, financing, investing

(Figure)Which of these transactions would be part of the financing section?

- inventory purchased for cash

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

(Figure)Which of these transactions would be part of the operating section?

- land purchased, with note payable

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

(Figure)Which of these transactions would be part of the investing section?

- land purchased, with note payable

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

Questions

(Figure)What categories of activities are reported on the statement of cash flows? Does it matter in what order these sections are presented?

Operating, Investing, Financing (always in this order).

(Figure)Describe three examples of operating activities, and identify whether each of them represents cash collected or cash spent.

(Figure)Describe three examples of investing activities, and identify whether each of them represents cash collected or cash spent.

Any transaction that is related to acquiring or disposing of long-term assets like land, buildings, equipment, stocks, bonds, or other investments. Can be cash spent for purchase of long-term assets, or cash collected from sale of long-term assets.

(Figure)Describe three examples of financing activities, and identify whether each of them represents cash collected or cash spent.

Exercise Set A

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- paid advertising expense

- paid dividends to shareholders

- purchased business equipment

- sold merchandise to customers

- purchased plant assets

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- borrowed from the bank for business loan

- declared dividends, to be paid next year

- purchased treasury stock

- purchased a two-year insurance policy

- purchased plant assets

Exercise Set B

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- collected accounts receivable from customers

- issued common stock for cash

- declared and paid dividends

- paid accounts payable balance

- sold a long-term asset for the same amount as purchased

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- purchased stock in Xerox Corporation

- purchased office supplies

- issued common stock

- sold plant assets for cash

- sold equipment for cash

Problem Set A

(Figure)Provide journal entries to record each of the following transactions. For each, also identify *the appropriate section of the statement of cash flows, and **whether the transaction represents a source of cash (S), a use of cash (U), or neither (N).

- paid $12,000 of accounts payable

- collected $6,000 from a customer

- issued common stock at par for $24,000 cash

- paid $6,000 cash dividend to shareholders

- sold products to customers for $15,000

- paid current month’s utility bill, $1,500

Problem Set B

(Figure)Provide journal entries to record each of the following transactions. For each, also identify: *the appropriate section of the statement of cash flows, and **whether the transaction represents a source of cash (S), a use of cash (U), or neither (N).

- reacquired $30,000 treasury stock

- purchased inventory for $20,000

- issued common stock of $40,000 at par

- purchased land for $25,000

- collected $22,000 from customers for accounts receivable

- paid $33,000 principal payment toward note payable to bank

Thought Provokers

(Figure)Use the EDGAR (Electronic Data Gathering, Analysis, and Retrieval system) search tools on the US Securities and Exchange Commission website to locate the latest Form 10-K for a company you would like to analyze. Submit a short memo that provides the following information:

- the name and ticker symbol of the company you have chosen

- the following information from the company’s statement of cash flows:

- amount of cash flows from operating activities

- amount of cash flows from investing activities

- amount of cash flows from financing activities

- the URL to the company’s Form 10-K to allow accurate verification of your answers

Glossary

financing activity cash business transaction reported on the statement of cash flows that obtains or retires financing investing activity cash business transaction reported on the statement of cash flows from the acquisition or disposal of a long-term asset operating activity cash business transaction reported on the statement of cash flows that relates to ongoing day-to-day operations

Operating vs. Investing vs. Financing Classifications

A deep dive into how cash flows are categorized under both IFRS and US GAAP, why it matters, and how analysts can spot classification tricks that inflate operating cash flows.

On this page

On this page

Enhance Your Learning:

Introductory Thoughts

I still remember the first time I tried to unravel a company’s statement of cash flows. I was sitting in a cramped office, sipping too much coffee, and trying to figure out why the firm’s operating cash flow looked suspiciously high. As it turned out, the company had been rather “creative” in choosing which cash items appeared in operating versus investing or financing categories. That small detail made a significant difference to the picture of health they presented to investors.

This section will walk you through the three pillars of the cash flow statement—Operating Activities, Investing Activities, and Financing Activities. We’ll explore IFRS vs. US GAAP treatments, highlight best practices and reporting pitfalls, and set you up to analyze potential manipulation. After all, the classification of cash flows is critically important for determining whether a firm’s core business is genuinely generating cash at a healthy rate.

Operating Activities (CFO)

Operating activities (often abbreviated as CFO) are the engine of most companies—the day-to-day churn of creating products, delivering services, and collecting payments from customers. Think about your own life: the money you make from your regular job is akin to the operating cash inflow, while the bills you pay for rent, groceries, and utilities are the operating outflows.

• Common Inflows: Cash from sales, fees for services, royalties, commissions.

• Common Outflows: Payments for inventory, payroll, rent, insurance, interest (under US GAAP), and taxes.

IFRS vs. US GAAP Differences for Operating Cash Flow

Under US GAAP, interest paid, interest received, and dividends received must be shown as part of CFO. Dividends paid, on the other hand, fall under financing activities. IFRS is more flexible:

• Interest Paid: IFRS allows classification as either CFO or Financing, provided the choice is applied consistently over time.

• Interest Received: IFRS allows classification as either CFO or Investing.

• Dividends Received: IFRS allows classification as either CFO or Investing.

• Dividends Paid: IFRS allows classification as either CFO or Financing.

Why does this matter? Because when a firm opts to move certain items—say interest paid—from operating to financing, the result can be a higher reported CFO. Investors who rely heavily on cash flow-based valuation models might be misled if they don’t notice these classification choices.

When to Be Cautious

If you ever see unusually high CFO relative to net income or to peer companies, that’s your cue to dig deeper. Check the footnotes: sometimes, IFRS-based statements reveal a footnote indicating that interest paid has been classified in financing or that a portion of dividends received has been moved to investing. All of these are legitimate under the rules, yet they can completely alter the impression of how much cash the core business is generating.

Investing Activities (CFI)

Here’s where the bigger ticket items usually show up—purchases and sales of long-term assets. In your personal life, this might be like buying a house or a car and then reselling it later. It doesn’t happen daily but can significantly impact your overall cash position when it does occur.

• Typical Inflows: Proceeds from selling property, plant, equipment (PP&E), intangible assets, or investment securities (not classified as cash equivalents).

• Typical Outflows: Purchases of PP&E, intangible assets, or investment securities.

IFRS vs. US GAAP Similarities and Differences

Under both US GAAP and IFRS, most purchases or sales of non-current assets or investments appear in investing activities. IFRS sometimes allows classification of interest received under CFI, whereas US GAAP does not.

Consider Redwood Interiors (a hypothetical furniture manufacturer). It invests in new machinery to streamline production, and that purchase is classified under investing activities. If Redwood Interiors later sells the machine at a profit or loss, that cash inflow also appears under investing. If Redwood Interiors decides to classify interest incoming from a short-term money-market investment, IFRS might let them classify it under investing, whereas US GAAP lumps it into operating. That difference alone can shift Redwood Interiors’ CFO metrics.

Hidden Warnings

Watch out for repeated negative or sharply fluctuating investing cash flows over time:

• Are the outflows genuinely for growth, such as expanding production capacity, or are they just replacing broken-down machinery?

• Could certain operating costs have been capitalized to artificially push them into investing? For instance, some firms might capitalize routine maintenance to bolster CFO.

If you suspect capitalizing routine operating costs, compare the firm’s depreciation expense and capital expenditure levels with industry averages or with their own historical data. Any out-of-line changes could raise eyebrows.

Financing Activities (CFF)

Financing is basically how the company pays for its big projects or returns money to its owners. If you start a small business and borrow money from a bank or give out shares to raise capital, that’s financing. Down the line, if you pay off part of the bank loan or repurchase shares, those are also financing activities.

• Typical Inflows: Proceeds from issuing bonds, new debt, or stock.

• Typical Outflows: Repayment of principal on loans, treasury stock repurchases, payment of dividends (under US GAAP), and so forth.

IFRS vs. US GAAP for Financing Activities

Under US GAAP, dividends paid must go here in financing. IFRS allows a choice between CFO and CFF for dividends paid, although the choice must be consistent year to year. A business that wants to boost CFO might place dividend payments in financing so that operating cash flow stays untouched. Alternatively, if they wish to demonstrate a specific financing profile, they could place it under operating (IFRS only).

Tailoring the Capital Structure

You may see lumps in financing cash flows related to big equity or debt issuance. For instance, if Redwood Interiors goes public, you’ll see a surge in CFF from the capital raise. Or if Redwood Interiors chooses to slash its debt significantly, you might observe a large outflow in a given period.

An abnormal pattern in dividends or share repurchases might signal a desire by management to manipulate share prices or to shed excess cash to maintain certain financial ratios (like return on equity). Financing data can also reveal how reliant the company is on external funding to keep afloat. Combining these insights with the CFO and CFI patterns can give you a holistic perspective on whether the firm’s growth is self-sustaining or debt-driven.

Discretion and Classification Games

One of the trickiest parts of analyzing cash flow statements is knowing where managers can bend the rules—especially under IFRS, which grants more leeway for classification choices. By selectively grouping certain items under investing or financing, management can inflate—or deflate—Operating Cash Flow.

Let’s look at how reclassification might occur:

flowchart TB A["Cash Flow from Operations (CFO)"] -- potential reclassification --> B["Cash Flow from Investing (CFI)"] A -- potential reclassification --> C["Cash Flow from Financing (CFF)"]

For instance, if interest expenses are thrown into financing under IFRS, CFO might surge. This is not illegal or “wrong,” but it does reduce comparability across firms using different accounting standards or different internal policies.

Detecting Potential Misclassifications

• Compare CFO to Net Income over multiple reporting periods. A chronic gap between net income and CFO might suggest that certain large operating expenses are parked in investing or financing.

• Look at footnotes and disclosures for explicit statements about classification policies. Changes in classification from year to year are a red flag that something might be up.

• Benchmark with peer companies. If you see that all your firm’s peers put interest received in operations, but your firm lumps it in investing (under IFRS), it might be legitimate, but it’s definitely worth investigating so you know why.

Assessing Overall Cash Flow Quality

Analysts often pay special attention to operating cash flow, because that category most strongly correlates with day-to-day sustainable business performance. Shifts in CFO can quickly raise an investor’s suspicion that the company is either thriving or facing liquidity troubles. When combined with net income, trending CFO reveals how well “paper profits” turn into actual cash.

Key Ratios and Red Flags

• CFO to Net Income: A ratio persistently below 1 could signal that much of the firm’s income is tied up in receivables or other non-cash items, or that operating items are capitalized.

• CFO to Capital Expenditures (CF CapEx): If CFO is barely covering capital spending, the firm may need additional debt or equity financing to keep growing.

• CFO to Total Debt: Lenders watch this ratio closely to see if the firm generates enough operating cash to service and repay obligations.

People sometimes say, “Cash is king.” In a sense, that’s true, but the classification of that cash can raise or lower the monarchy’s standing. So for the CFA Level II exam, you need a handle on how each section (CFO, CFI, CFF) is defined under IFRS and US GAAP, plus a sense of how to detect potential misclassification or fuzzy accounting.

Actionable Steps for Analysts

• Align the classification approach with IFRS or US GAAP guidelines and confirm consistency from year to year.

• Investigate big swings in CFO, particularly if net income remains relatively stable or vice versa.

• Check the footnotes for any explicit mention of reclassification. IFRS-based companies might detail how they treat interest and dividends.

• Cross-check with peer companies. Are they all classifying interest in CFO while your target firm chooses investing? Why?

• Build a multi-period comparison or prepare a table of CFO, CFI, CFF to see trends. Also note if the firm changes classification approaches after a major shift in management or ownership.

A Quick Example

Suppose Redwood Interiors reports $300,000 in net income. Its doors are seemingly flying off the shelves. But when you dig into the cash flow statement, you notice CFO is only $150,000, while CFI is negative $400,000 due to new factory equipment. Meanwhile, Redwood Interiors classifies $50,000 of interest payment as financing under IFRS. If Redwood Interiors had used US GAAP, that $50,000 would reduce CFO further to $100,000, a big difference in perceived operating strength.

If Redwood Interiors also paid dividends of $10,000, IFRS might show that $10,000 outflow under CFO or under financing. Again, the choice changes how robust CFO looks. This example underscores how classification can tilt analyst perceptions and key coverage ratios.

Best Practices and Common Pitfalls

• Best Practice: Keep an eye on the net effect, not just one line item. Sometimes, a small reclassification from CFO to CFI might have a huge effect on operating metrics or coverage ratios.

• Pitfall: Taking CFO at face value—especially if a company transitions from US GAAP to IFRS or vice versa, or if they adopt new IFRS guidelines that allow more classification flexibility. Without adjusting, you might incorrectly rank the firm’s performance.

• Best Practice: Document classification policies in your model. If you’re building a DCF (discounted cash flow) analysis, note any classification quirks so you don’t inadvertently double count or miscount.

• Pitfall: Not exploring year-over-year classification changes. If the footnotes show that last year’s interest expense was in CFO but this year it’s in CFF, that big jump in CFO might simply be a result of reclassification, not genuine improvement.

Final Thoughts

When it comes to analyzing and interpreting the statement of cash flows, the devil is in the details. Things like interest and dividend classification can dramatically shift a company’s reported operating cash flow, and IFRS offers more wiggle room than US GAAP does. For your Level II exam—and for real-world investment decisions—take the time to dissect these classifications, read a company’s footnotes thoroughly, and compare the firm’s policies with industry norms. It can save you from being caught off guard by artificially rosy metrics and let you focus on the business fundamentals that really matter.

References

• CFA Institute (2025). CFA® Program Curriculum, Level II, Volume 4: Financial Statement Analysis. CFA Institute.

• IAS 7, Statement of Cash Flows, International Financial Reporting Standards (IFRS).

• FASB Accounting Standards Codification (ASC) 230, Statement of Cash Flows.

• White, G. I., Sondhi, A. C., & Fried, D. (2019). The Analysis and Use of Financial Statements (3rd ed.).

Show Off Your Cash Flow Classification Skills

### Which item typically belongs to Operating Activities under US GAAP? – [ ] Proceeds from issuing bonds. – [x] Cash received from customers. – [ ] Cash paid to acquire machinery. – [ ] Dividends paid to shareholders. > **Explanation:** Under US GAAP, operating cash flows primarily include transactions connected to the firm’s principal revenue-generating activities. Receiving cash from customers is part of the day-to-day operations. ### Under IFRS, which statement regarding interest and dividend classification is TRUE? – [x] Interest paid may be either operating or financing, and dividends paid may be operating or financing. – [ ] Dividend paid must always be operating. – [ ] Interest received always falls under operating activities. – [ ] Dividends received must always be under operating activities. > **Explanation:** IFRS permits more flexibility. Interest paid can be classified as operating or financing (as long as it’s consistent), and dividends paid may be operating or financing. Similar discretion applies to interest received or dividends received, which can be operating or investing. ### A firm that seeks to inflate Operating Cash Flow under IFRS might classify which of the following under financing? – [ ] Cash collected from customers. – [ ] Proceeds from the sale of equipment. – [x] Interest payments on debt. – [ ] Payment of salaries. > **Explanation:** By shifting interest payments from operating to financing, the company can artificially boost CFO. IFRS allows that choice; US GAAP does not. ### Which ratio best demonstrates how effectively an entity converts accrual-based earnings into cash? – [x] CFO to Net Income. – [ ] Debt to Equity. – [ ] Current Ratio. – [ ] Price to Earnings. > **Explanation:** The CFO to Net Income ratio indicates how closely net income aligns with actual cash generated by operations. A consistent ratio is desirable; a large deviation suggests potential aggressive revenue recognition or capitalizing expenses. ### Under US GAAP, dividends received are always classified under: – [ ] Investing Activities. – [ ] Financing Activities. – [x] Operating Activities. – [ ] Either operating or financing, depending on management’s discretion. > **Explanation:** US GAAP is strict on this point. Dividends received must be recorded under operating activities. ### If a company uses IFRS and pays dividends, which of the following is an acceptable classification? – [x] Dividends paid as either operating or financing. – [ ] Dividends paid as either operating or investing. – [ ] Dividends paid must always be operating. – [ ] Dividends paid must always be investing. > **Explanation:** IFRS permits classification of dividends paid in either operating or financing, as long as it’s applied consistently. ### A large negative balance in Investing Activities might indicate: – [x] Intensive capital expenditures or significant acquisitions. – [x] Potential capitalizing of what could be operating expenditures. – [ ] Plans to issue new shares. – [ ] Exaggerated CFO from reclassification of dividends. > **Explanation:** A large negative CFI often implies the company is spending heavily on assets (which can be good for growth) or possibly capitalizing routine expenses. Always compare with footnotes and the firm’s historical data. ### Which of the following would you scrutinize if Operating Cash Flow consistently exceeds Net Income? – [ ] Steady classification of dividends received as investing. – [ ] Low capital expenditures. – [x] Any changes in classification of interest or dividends under IFRS. – [ ] The issuance of common stock. > **Explanation:** If OCF is persistently outpacing net income, you might suspect shifting interest or dividends from operating to other sections under IFRS, or conservative revenue recognition that consistently defers expenses. ### All else being equal, how would reclassifying interest paid from operating to financing (under IFRS) likely affect the CFO? – [x] Increase CFO. – [ ] Decrease CFO. – [ ] Have no effect on CFO. – [ ] CFO may increase or decrease depending on other items. > **Explanation:** If interest paid moves from operating to financing, it lowers financing outflows but simultaneously boosts CFO, since less cash outflow is placed under operating. ### True or False: The classification of cash flows cannot influence key financial ratios. – [ ] True – [x] False > **Explanation:** Classification can significantly shift CFO, which affects metrics like the cash flow-to-debt ratio, coverage ratios, and overall impressions of operating performance.

Sunday, June 22, 2025

Friday, March 21, 2025

Important Notice: FinancialAnalystGuide.com provides supplemental CFA study materials, including mock exams, sample exam questions, and other practice resources to aid your exam preparation. These resources are not affiliated with or endorsed by the CFA Institute. CFA® and Chartered Financial Analyst® are registered trademarks owned exclusively by CFA Institute. Our content is independent, and we do not guarantee exam success. CFA Institute does not endorse, promote, or warrant the accuracy or quality of our products.

https://spscc.pressbooks.pub/financialaccountingoriginal/chapter/differentiate-between-operating-investing-and-financing-activities/https://financialanalystguide.com/cfa-level-2/volume-4-financial-statement-analysis/21/1/