Examples of Operating, Investing, and Financing Activities in Cash Flow Statements

Welcome to our blog post on examples of operating, investing, and financing activities in cash flow statements! If you’re curious about how companies report their cash flows and want to gain a better understanding of the direct and indirect methods, you’ve come to the right place. In this article, we’ll explore the various types of activities that fall into these categories and provide insights into why the indirect method is preferred. We’ll also touch on topics like non-cash transactions, the preparation of cash flow statements, and the recommended approach by the Financial Accounting Standards Board (FASB).

Tracking cash flow is an essential aspect of evaluating a company’s financial health. By analyzing the cash flow statement, investors, analysts, and stakeholders can gain valuable insights into how a company generates and uses its cash. Whether you’re an aspiring accountant, a business owner, or simply curious about the financial operations of companies, understanding operating, investing, and financing activities is crucial.

So, let’s dive into the world of cash flow statements and explore the different activities that come under the operating, investing, and financing categories. By the end of this article, you’ll have a better understanding of how these activities are reported and how they impact a company’s overall financial performance. Let’s get started!

Examples of Operating, Investing, and Financing Activities

Operating, investing, and financing activities are three key aspects of a company’s financial activities. Each represents a distinct category of financial transactions that contribute to a company’s overall financial health and performance. Let’s take a closer look at some examples of each:

Operating Activities

Operating activities are the day-to-day business activities that generate revenue and incur expenses for a company. These activities are essential for a company to run and maintain its operations smoothly. Here are a few examples of operating activities:

Sales and Purchases

One of the primary operating activities is the sale of goods or services. For instance, if you own a computer store, selling laptops to customers would be considered an operating activity. On the flip side, purchasing inventory or raw materials to manufacture products to meet customer demand also falls under this category.

Payment of Salaries and Wages

Another example of an operating activity is the payment of salaries and wages to employees. Your employees’ hard work and dedication contribute to your company’s functioning, and compensating them for their efforts is an essential part of the day-to-day operations.

Payment of Suppliers

When you buy goods or services from suppliers, you need to make timely payments to them. This payment represents an operating activity as it directly impacts your company’s cash flow and ensures the continuous supply of goods or services required for your business operations.

Investing Activities

Investing activities involve the acquisition or disposal of long-term assets that are not intended for immediate sale. These activities aim to increase the company’s long-term value rather than generate immediate revenue. Here are a couple of examples of investing activities:

Purchase of Property, Plant, and Equipment

Investing in tangible assets like property, plant, and equipment is a common investing activity. For instance, if you decide to buy a new office space or upgrade your machinery, the cash outflow associated with these purchases would fall under this category.

Acquiring Investments

Investments in stocks, bonds, or other financial instruments are also considered investing activities. For example, if your company invests in shares of another company or buys government bonds, these transactions would be classified as investing activities.

Financing Activities

Financing activities involve obtaining funds to support a company’s operations or investments and repaying those funds over time. Here are a couple of examples of financing activities:

Obtaining Loans

When a company takes out a loan from a bank or other financial institution to fund its operations or invest in new projects, it is considered a financing activity. The funds received from the loan increase the company’s liabilities, and repayments decrease them.

Issuing Stock

Companies can raise funds by issuing shares of stock to investors. This act of selling ownership in the company to raise capital is known as an equity financing activity. It helps companies secure funds for various purposes, such as expansion or debt repayment.

Now that we have explored examples of operating, investing, and financing activities, it’s clear that each category encompasses distinct financial transactions. By understanding these activities and their impact on a company’s financial statements, you can gain valuable insights into a company’s overall financial performance.

FAQ: What are examples of operating investing and financing activities?

Welcome to our comprehensive FAQ-style guide on operating, investing, and financing activities! In this section, we’ll answer some common questions about these activities to help you gain a better understanding. So, let’s dive right in!

What are examples of operating investing and financing activities

Operating activities include the day-to-day running of a company. Examples of operating activities can include cash received from customers, cash paid to suppliers, wages paid to employees, and expenses such as rent and utilities.

Investing activities, on the other hand, involve the acquisition or sale of assets. Examples of investing activities can include the purchase or sale of property or equipment, investments in securities or other companies, and loans made to other entities.

Financing activities cover the ways a company raises capital and repays its debt. Examples of financing activities can include issuing or repurchasing stock, borrowing or repaying loans, and paying dividends to shareholders.

Do most companies use the direct or indirect method

When it comes to preparing a statement of cash flows, most companies use the indirect method. This method starts with net income and adjusts for non-cash items and changes in working capital to arrive at cash from operating activities.

What are the steps to prepare a cash flow statement

Preparing a cash flow statement involves a few key steps:

- Begin with the net income reported on the income statement.

- Add back any non-cash expenses such as depreciation and amortization.

- Adjust for changes in working capital, including accounts receivable, accounts payable, and inventory.

- Account for investing activities such as the purchase or sale of assets.

- Account for financing activities such as issuing or repurchasing stock, or taking out loans.

- Calculate the net increase or decrease in cash and cash equivalents.

Which of the following activities is an example of an operating activity

An example of an operating activity is cash received from customers. This would be considered part of a company’s daily operations.

What is a direct and indirect cash flow statement

A direct cash flow statement provides a detailed breakdown of cash inflows and outflows from operating activities. This method directly lists the cash flow items, such as cash received from customers and cash paid to suppliers.

An indirect cash flow statement starts with net income and adjusts for non-cash items and changes in working capital to arrive at cash from operating activities.

Why is the indirect method preferred

The indirect method is often preferred because it is simpler and less time-consuming than the direct method. It allows companies to use their existing financial statements as a starting point and make adjustments from there.

Is accounts payable operating, investing, or financing

Accounts payable is considered an operating activity. It represents the amount a company owes to its suppliers for goods and services received.

Who prepares the cash flow statement

The cash flow statement is typically prepared by the company’s accounting or finance department. It requires a good understanding of the company’s financial transactions and the ability to analyze and interpret financial data.

What are non-cash transactions on the cash flow statement

Non-cash transactions on the cash flow statement refer to activities that do not involve an actual movement of cash. Examples of non-cash transactions can include the issuance of common stock in exchange for assets, the conversion of debt into equity, and the transfer of assets or liabilities without any exchange of cash.

What is the difference between an indirect and a direct cash flow statement

The main difference between an indirect and a direct cash flow statement lies in how the operating activities section is presented.

In the indirect method, the operating activities section starts with net income and adjusts for non-cash items and changes in working capital. It provides a reconciliation of net income to cash provided (or used) by operating activities.

In the direct method, the operating activities section directly lists the cash flow items, such as cash received from customers and cash paid to suppliers, without starting from net income. It provides a more detailed view of the cash flows related to operating activities.

When equipment is sold for cash, is the amount received reflected as a cash inflow or outflow

When equipment is sold for cash, the amount received is reflected as a cash inflow in the cash flow statement. This inflow would be categorized under the investing activities section.

Why does the FASB recommend the direct method over the indirect method

While the Financial Accounting Standards Board (FASB) allows both the direct and indirect methods for presenting operating activities on the cash flow statement, they do recommend the direct method if the necessary information is available. The direct method provides more transparency and a clearer picture of the company’s cash flow from operating activities.

What is the operating cash flow formula

The operating cash flow formula calculates the cash generated from a company’s core operations. It is calculated by taking net income and adjusting for non-cash expenses and changes in working capital. The formula is as follows:

Operating Cash Flow = Net Income + Non-cash Expenses (e.g., depreciation) +/- Changes in Working Capital

What is the indirect method

The indirect method, also known as the reconciliation method, is a technique used to convert net income into net cash provided (or used) by operating activities. It involves adjusting net income for non-cash expenses, changes in working capital, and other adjustments to arrive at the cash flow from operating activities.

We hope this FAQ-style guide has provided you with valuable insights into the examples of operating, investing, and financing activities. Understanding these activities is crucial for analyzing a company’s financial health and overall performance. If you have any further questions or need additional information, feel free to reach out to us. Happy investing!

Financing Activities

Financing activities are the different transactions that involve the movement of funds between the company and its investors, owners, or creditors to achieve long-term growth and economic goals and have an effect on the equity and debt liabilities present on the balance sheet; Such activities can be analyzed through the cash flow from finance section in the cash flow statement of the company.

Financing activities cash flow refers to the act of raising money or returning this raised money by promoters or owners of the firm to grow and invest in assets like purchasing new machinery, opening new offices, hiring more workforce, etc. These transactions are normally part of a long-term growth strategy and hence affect the long-term assets and liabilities of the firm.

Financing Activities Explained

Financial activities primarily involve transactions with investors and creditors, influencing the overall financial health and stability of the organization.

One facet of financing activities is equity financing, where a company raises funds by issuing shares of its stock. This can occur through initial public offerings (IPOs) or subsequent stock offerings. Investors, in return, become shareholders and have ownership stakes in the company, sharing in its profits and losses.

On the other hand, debt financing involves raising capital by borrowing funds. This can take the form of loans, bonds, or other debt instruments. The company commits to repaying the borrowed amount along with interest over a specified period. Bond issuances, for example, are a typical means of long-term debt financing.

Financing activities also encompass the distribution of profits to shareholders through dividends. Additionally, companies may engage in share repurchases, buying back their stock from the market. These actions impact the company’s equity structure and can signal confidence in its financial standing.

Understanding and effectively managing financing activities accounting are paramount for businesses to optimize their capital structure, strike a balance between debt and equity, and ensure sustainable growth while meeting financial obligations. It is a delicate dance that financial managers must navigate to secure the necessary resources for operations and strategic initiatives.

Types

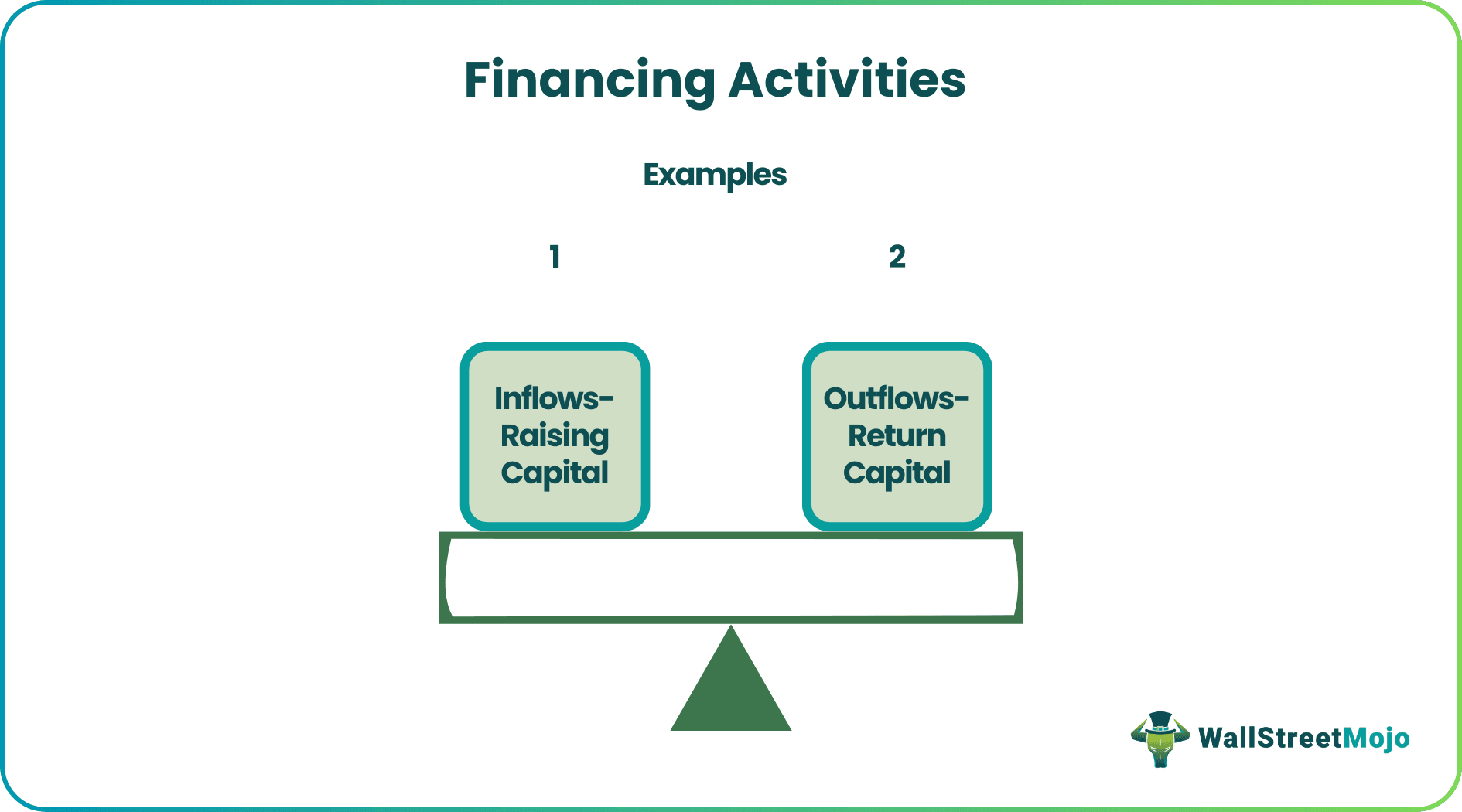

Let us understand the different types of investments that lead to financing activities cash flow through the detailed discussion below.

Inflows – Raising Capital

- Equity Financing: This corresponds to selling your equity to raise capital. Here the money is raised without obligation to pay any principal or interest but at the cost of ownership. It’s an inflow that, on its face, looks like easy money but may prove very costly in the long term. Sometimes, because of a growing business, you might pay more interest than the prevailing market rates.

- Debt Financing: Another way to raise capital is by issuing long term debt bonds. This, in contrast to equity financing, does not dilute ownership but makes the firm liable to pay fixed interest and return the money within the promised timeframe, normally for 10 or 20 years.

- If the firm is a not-for-profit organization, donor contributions can also be part of the financing.

Outflows – Return Capital

- Repayment of Equity: When owners have enough wealth in-store, they would like to buyback the company stock and increase their ownership. They can do so in multiple ways like – buying stocks from an open market, bringing offer for sale, or proposing a buyback.

- Repayment of Debt: Like any fixed deposit, firms must repay the debt after a definite period as promised at the time of the issue.

- Dividend Payment: This is a mechanism by which firms reward their shareholders and share their profits. Since these are subject to tax, firms sometimes use the capital to buy back shares from the shareholders by bringing a buyback offer. This decreases the number of shares in the market and hence increases the earnings per share.

How to Record?

The Financing activities accounting examples listed above are recorded in the cash flow statement of the firm. Diagrammatically, it can be explained as:

Since financing activity is all about cash inflows and cash outflows recorded in the cash flow statement of the firm, they can be calculated by adding all inflows and outflows individually and then taking an algebraic sum of the two derived terms.

Consider the following example of a firm that undergoes the following financing activities:

Advantages

Let us understand the advantages of financial activities cash flow through the explanation below.

- Financing activities provide much-needed fuel for the firms to grow and expand into new markets. It is easy to imagine what would have happened to major internet giants of today like Facebook or Google, or even our homegrown OLA, had they not been able to raise money for their expansion plans. Companies short of capital might lose out on new opportunities and new customers.

- It provides valuable insight to the investors about the firm’s financial health. For example, financing activity like the buyback of shares regularly indicates that promoters are very optimistic about the growth story and want to retain ownership. This is why Indian IT majors like Infosys and TCS brought consecutive buybacks in 2 years, and the same was cheered by the investors. On the other hand, if a firm is readily diluting its equity, investors might assume that it is going through financial distress and facing issues in raising capital from banks or other lenders.

Disadvantages

Despite the various advantages listed in the section above and throughout the article, there are a few factors that prove to be a disadvantage. Let us understand them through the points below.

- Financing activities accounting is often in the interest of regulators as they are often attentive to how the money has been financed and what it is used for. Firms should be vigilant during these operations as a slight mistake can invite regulatory scrutiny, leading to a lengthy legal hassle. Walmart buying Flipkart stake was one such financing activity example.

- More than what amount of capital has been raised in consideration of how this capital has been raised or returned to the investors. There is always a tax implication that these firms’ accountants should consider. For example, financing activities like paying dividends attract tax, but share buyback does not. Though differing in the long term, these mechanisms are similar in the short term, i.e., rewarding stock owners.

- Diluting equity too much and not redeeming it back might become an example of a hostile takeover.

Financing Activities Vs Investing Activities

Let us understand the differences between financing activities accounting and investing activities through the comparison below.

Financing Activities

- Financing activities involve transactions related to obtaining funds to support the company’s operations and growth.

- Companies engage in financing activities to shape their capital structure, balancing debt and equity to meet financial obligations and optimize growth.

- Includes equity financing through stock issuances and debt financing through loans or bond issuances.

- Payment of dividends to shareholders is considered a financing activity, as it involves using a portion of profits to reward investors.

- Buying back company shares from the market is a financing activity, impacting the company’s equity structure.

Investing Activities

- Investing activities involve the acquisition and disposal of long-term assets, such as property, equipment, and investments.

- Companies make investment decisions to enhance their operational capabilities, expand into new markets, or generate returns on investments.

- Capital expenditures, such as purchasing machinery or building facilities, are considered investing activities.

- Selling assets, whether it’s real estate or investments, is part of investing activities and can generate cash inflows.

- Investing activities are focused on generating long-term value for the company by strategically deploying resources in ventures that contribute to its growth and profitability.

Create a Full Dynamic Financial Model in 2 Days (6 hours) | Any Graduate Or Professional is eligible | Build & Forecast IS, BS, CF from Scratch.

Join WallStreetMojo YouTube

The Exact Training Used by Top Investment Banks | FM, DCF, LBO, M&A, Accounting, Derivatives & More | $2400+ in Exclusive Benefits | 100+ Wall Street-Level Skills.

Join WallStreetMojo Instagram

Boost Productivity 10X with AI-Powered Excel | Save Hours, Eliminate Errors | $300+ in Exclusive Bonuses | Advanced Data Analysis & Reporting with AI.

Join WallStreetMojo LinkedIn

![]()

Master Excel, VBA, PowerBI Like a Pro | 70+ Hours of Expert Training | Real-world Excel applications | Earn Your Certification & Land High-Paying Roles!

https://www.appgecet.co.in/examples-of-operating-investing-and-financing-activities-in-cash-flow-statements/https://www.wallstreetmojo.com/financing-activities/